Follow us on LinkedIn

Companies use assets to generate revenues. Usually, they include fixed assets, which are crucial to running operations. Most of these assets contribute to the production of goods or services. However, some assets may also be critical in running the administrative side of the business. One of those assets includes office equipment.

What is Office Equipment?

Office equipment is a fixed asset that companies use for administrative purposes. The equipment used in this category fall under the office equipment accounts. Usually, this account holds the acquisition cost of the fixed assets classified in the category. Office equipment includes items that companies intend to use for the long term. Therefore, these have a similar accounting treatment as other fixed assets.

Office equipment falls under non-current assets in the balance sheet. Usually, companies classify these as property, plant, and equipment. The accounting treatment of office equipment also falls under the scope of IAS 16. On the other hand, office equipment depreciation becomes a part of the income statement. For most companies, this category includes the following assets.

- Office furniture

- Computers

- Networking and communication equipment

- Printers, copiers, and scanners

- Security systems

What is Office Equipment depreciation?

Office equipment depreciation is a term that relates to the depreciation charged on those assets. This depreciation is similar to that calculated on other fixed assets. As mentioned, office equipment falls under the scope of IAS 16. Therefore, companies cannot expense them out in the income statement when acquired. Instead, they must spread those costs over the useful life.

The accounting for office equipment depreciation is a part of IAS 16. When a company acquires these assets, it must determine their useful life. Similarly, if the equipment has a scrap or salvage value, it must also consider it. Once these estimates are available, the company can calculate the office equipment depreciation.

How to calculate the Office Equipment depreciation?

Companies can calculate office equipment depreciation under several approaches. Usually, companies opt for the straight-line method of depreciation. However, some companies may also use the declining or double-declining method. These methods to office equipment depreciation produce the best results. Nonetheless, the company must use a similar approach to depreciate all equipment within this category.

Companies can use the following formula to calculate office equipment depreciation.

Depreciation = (Office equipment cost – Office equipment salvage value) / Useful life

The above formula applies to the straight-line method of depreciating assets. With this method, companies get a fixed depreciation amount for each year. In contrast, companies can also calculate the double-declining depreciation as follows.

Depreciation = (Office equipment carrying value – Office equipment salvage value) / Useful life x 2

Example

A company, Blue Co., acquires computers for office use, which fall under office equipment. These computers cost $10,000 with an estimated useful life of 5 years. Historically, the company has used straight-line depreciation for its office equipment. Therefore, it must also use the same approach to calculate the depreciation on these computers.

Blue Co. calculates the office equipment depreciation for the computers as below.

Depreciation = (Office equipment cost – Office equipment salvage value) / Useful life

Depreciation = ($10,000 – $0) / 5 years

Depreciation = $2,000

Blue Co. can charge this amount in the accounts each year. The company can use the following journal entries for the office equipment depreciation.

| Dr | Depreciation | $2,000 |

| Cr | Accumulated depreciation | $2,000 |

Conclusion

Office equipment includes assets that companies acquire for office use. These may consist of various items, as listed above. For these assets, companies must use IAS 16 as a guide which applies to all property, plant, and equipment. Companies must also calculate depreciation on the office equipment. Consequently, they can use several approaches, including straight-line, declining, and double-declining methods.

Further questions

What's your question? Ask it in the discussion forum

Have an answer to the questions below? Post it here or in the forum

VICTORIA, British Columbia — Vecima Networks Inc. (TSX: VCM) announced today that Dell’Oro Group has recognized the company as the 2023 market share leader in two Distributed Access Architecture (DAA) segments – Remote Optical Line Terminals (R-OLT) and Remote MACPHY (R-MACPHY). Dell’Oro Group named Vecima…

Net Income Per Share Increased by 184% Compared to 2022 CALGARY, Alberta, April 24, 2024 (GLOBE NEWSWIRE) — Tornado Global Hydrovacs Ltd. (“Tornado” or the “Company”) (TSX-V: TGH; OTCQX: TGHLF) today reported its audited consolidated financial results for the year ended December 31, 2023, with…

Lire en français OTTAWA, April 24, 2024 (GLOBE NEWSWIRE) — The Canada Plastics Pact (CPP), in partnership with the National Zero Waste Council, has released guidance for industry to take urgent measures to eliminate unnecessary and problematic plastics. The guidance includes a list of 13…

VANCOUVER, British Columbia, April 24, 2024 (GLOBE NEWSWIRE) — Highland Copper Company Inc. (TSXV: HI; OTCQB: HDRSF) (“Highland” or the “Company”) is pleased to announce that White Pine Copper LLC., its joint venture with Kinterra Copper USA LLC, has successfully completed its winter drilling program…

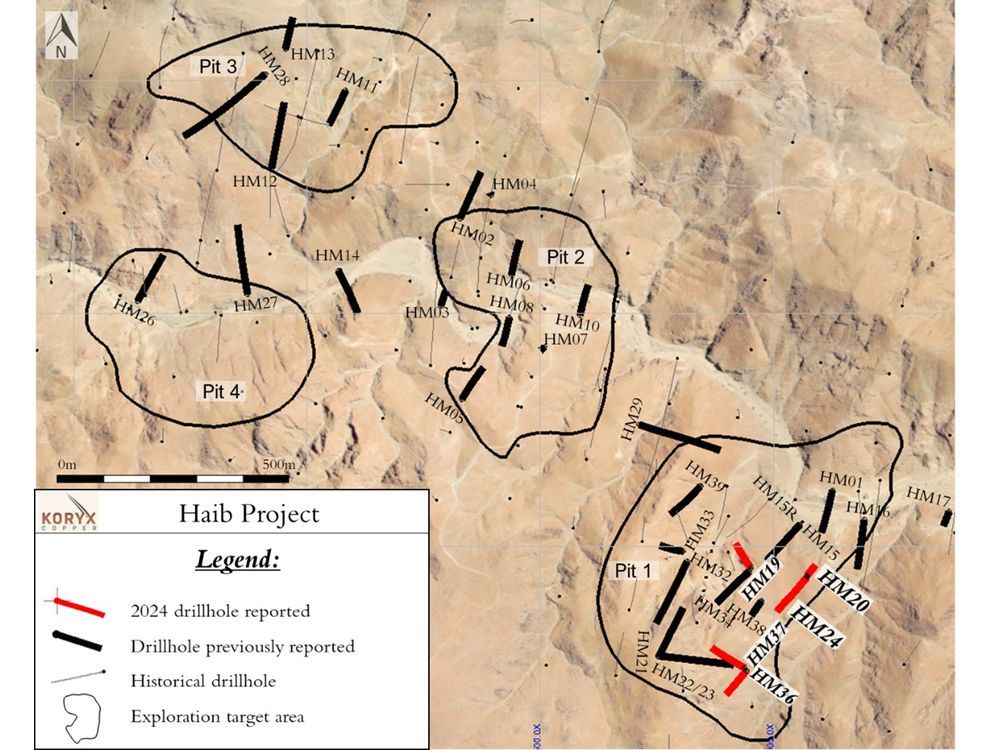

INCLUDING 2 METERS AT 3.95% CU EQ AND MULTIPLE 2 METRES INTERSECTIONS OVER 1.00% CU EQ Significant copper and molybdenum intersections include: HM19: 116 m from near surface @ 0.54% CuEq HM20: 26.00 m @ 0.44% CuEq HM24: 44.00 m 0.32% CuEq HM36: 207 m…