Last year, in a post entitled Credit Derivatives-Is This Time Different we wrote about credit derivatives and their potential impact on the markets. Since then, they have started attracting more and more attention. For example, Bloomberg recently reported that collateralized loan obligations (CLO), a type of complex credit derivatives, are becoming a favorite financing vehicle for corporate America.

…Investors haven’t been able to get enough of the repackaged corporate loans known as collateralized loan obligations. That intense demand, is allowing the managers that put these securities together to sell off pieces of CLOs that by law they previously had to hang on to. These sales are the crest of what could be a $7 billion wave of such deals. Read more

As reported by the Washington Post, money raised from these CLOs is used to finance corporate stock buybacks and dividend payouts.

The most significant and troubling aspect of this buyback boom, however, is that despite record corporate profits and cash flow, at least a third of the shares are being repurchased with borrowed money, bringing the corporate debt to an all-time high, not only in an absolute sense but also in relation to profits, assets and the overall size of the economy.

In recent years, moreover, a greater part of corporate borrowing has come in the form of bank loans that are quickly packaged into securities known as CLOs, or collateralized loan obligations, which are sliced and diced and sold off to sophisticated investors just as home loans were during the mortgage bubble. Bloomberg News recently reported that pension funds and insurance companies, particularly those in Japan, can’t get enough of the CLOs because of the higher yields that they offer. Wells Fargo estimates that a record $150 billion will be issued this year, roughly double last year’s issuance. And as happened with the late-cycle home mortgages in 2007 and 2008, analysts are noticing a marked decline in the quality of loans in the CLO packages, with three-quarters of them now without the standard covenants designed to reduce the chance of default. Read more

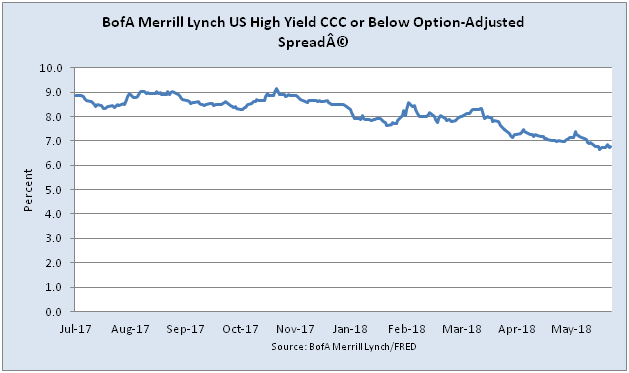

But how risky are these collateralized loan obligations?

In the current market environment, it’s difficult to evaluate the riskiness of these CLOs. First of all, Value at Risk (VaR), a popular risk measure used by many financial institutions to quantify the risks and manage economic capital, has been developed and tested in a low-interest rate and low-volatility environment. This makes the VaR vulnerable to future change in the market environment.

Second, in the calculation of VaR for a credit derivative portfolio, we would have to determine the probabilities of default (PD) and loss given default (LGD) of the borrowers. Both of these quantities are difficult to estimate. Furthermore, the correlation between PD and LGD is not constant and will likely increase during a market stress.

All of these factors make the VaR less accurate. Consequently, managing the risks of a CLO portfolio is a non-trivial task. A slight change in the market environment can lead to damaging consequences.

Further questions

What's your question? Ask it in the discussion forum

Have an answer to the questions below? Post it here or in the forum

The WSJ Dollar Index was down 0.4% to 98.73 — down for three of the past four trading days.