The Black–Scholes-Merton model is the most frequently used option pricing model in the financial industry. However, it made use of assumptions that are not always realistic. A crucial assumption of the Black-Scholes-Merton model is a frictionless and elastic market. In other words, it assumes that there are no barriers to buying or selling securities and that investors can instantly buy or sell an asset at the prevailing market price. The markets are, however, not frictionless, and the buying and selling of securities can have an impact on the markets. This is often called a feedback loop.

Reference [1] examined how the delta hedging in the foreign exchange market can have an impact on the market volatility,

We theoretically model and empirically quantify the feedback effect of delta hedging for the spot market volatility of the forex market. We start from an economy with two types of traders, an aggregated option market maker (OMM) and an aggregated option market taker (OMT), whose exposures reflect the total outstanding positions of all option traders in the market. A different hedge ratio of the OMM and OMT leads to a net delta hedge activity, which introduces market friction.

The authors concluded that delta hedging by the market makers increases volatilities,

The gamma exposure of the OMM turns out to be highly significant for the spot market volatility and, as expected, the spot market volatility is increased with the OMM’s short gamma exposure. Quantitatively, a negative gamma exposure of the OMM of approximately -1000 billion USD (which is around what we observe from our reconstructed OMM data) leads to an absolute increase in volatility of 0.7% in EURUSD and 0.9% in USDJPY.

The findings are consistent with our experience, as it’s widely acknowledged that feedback effect (or reflexivity) exists in the financial markets. This article provided a formal proof. It would be interesting to see a similar study on the leveraged Exchange-Traded Funds.

References

[1] B. Anderegga, F.Ulmann, D. Sornette, The impact of option hedging on the spot market volatility, Journal of International Money and Finance, 124, 2022, 102627

Further questions

What's your question? Ask it in the discussion forum

Have an answer to the questions below? Post it here or in the forum

SASKATOON, Saskatchewan — Cameco (TSX: CCO; NYSE: CCJ) was informed by our partner, National Atomic Company Kazatomprom JSC (Kazatomprom), and Joint Venture Inkai LLP (JV Inkai), that as of January 1, 2025, JV Inkai has suspended production activity. On December 31, 2024, JV Inkai formally…

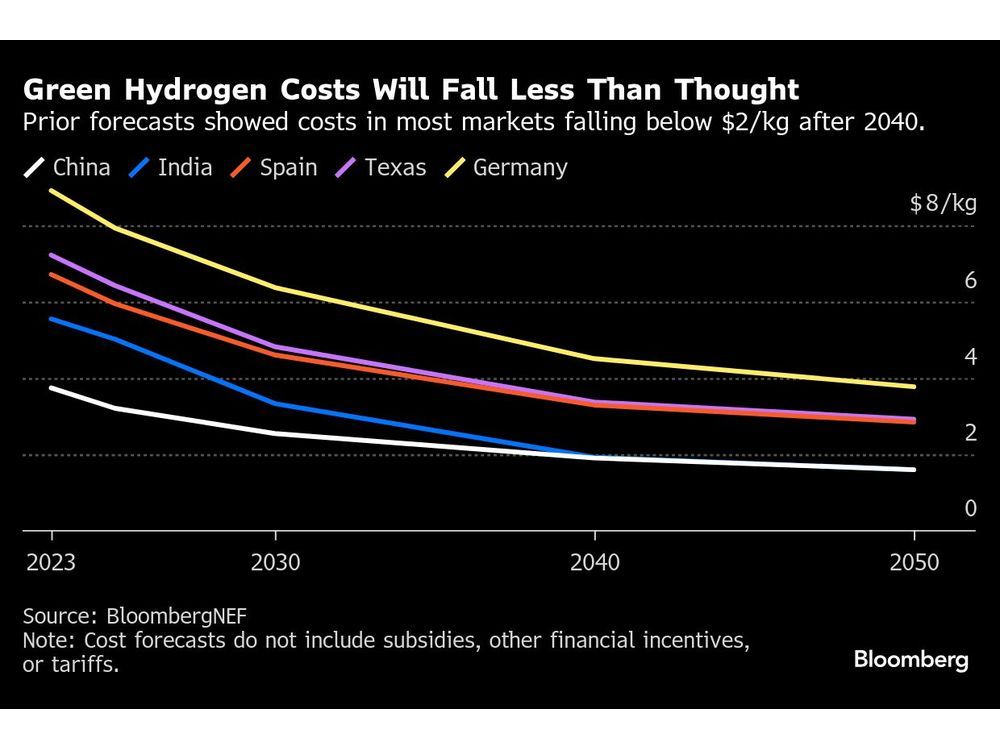

With Trump in the White House, the prospect of a trade war and $86 billion in unspent funds, climate venture capitalists are realigning their investment strategies.