Follow us on LinkedIn

An auditor’s opinion is a statement that auditors provide after auditing a company’s financial statements. Usually, this process involves examining these statements and collecting audit evidence. Based on this process, auditors come to a conclusion to form an opinion. Usually, this conclusion entails ensuring the financial statements are free from material misstatements. Similarly, it includes commenting on fair and true presentation.

There are different types of audit opinions that auditors may provide. Usually, auditors state an unmodified audit opinion, which assures stakeholders of the integrity and objectivity of the financial statements. However, auditors may also give an unmodified opinion. This opinion has three types, including qualified opinion, adverse opinion, and disclaimer of opinion.

What is the Disclaimer Audit Opinion?

Auditors consider two factors crucial to the audit opinion they provide. The first includes the financial statements being free from material misstatements. The second entails collecting sufficient appropriate audit evidence related to items in those statements. The disclaimer of audit opinion relates to the audit evidence that auditors obtain. It differs from other qualified audit opinions.

Auditors provide the disclaimer audit opinion when they can’t obtain sufficient appropriate audit evidence. There are various reasons why auditors cannot collect audit evidence. Sometimes, it may include the management not cooperating. In other circumstances, it may also involve the audit evidence not existing at all. Whatever the reason, if auditors cannot obtain audit evidence to support their audit opinion, they will provide the disclaimer audit opinion.

The unavailability of audit opinion may also fall under the qualified audit opinion. However, auditors use the disclaimer audit opinion when the impact of the audit evidence is pervasive. In auditing, a matter becomes pervasive when its effects spread to the financial statements as a whole. In some cases, it may also include misstatements being a substantial portion of those statements.

How does the Disclaimer Audit Opinion work?

The audit process involves the auditors obtaining sufficient appropriate evidence. Usually, clients provide supporting documents or information with their transactions or events. In some cases, however, it may not be available. For example, a company may not have the supporting documents required to back up its sale transactions. Sometimes, clients may also have evidence, but the auditors may not consider it sufficiently appropriate.

If the effect of the unavailable sufficient appropriate audit evidence is immaterial, auditors may ignore it. Similarly, if they have a material impact, the auditors may provide a qualified opinion. In some cases, it may be pervasive. Therefore, the auditors must use the disclaimer audit opinion. With this opinion, auditors state that they couldn’t obtain audit evidence to form an opinion.

A disclaimer audit opinion does not involve providing or expressing an opinion. Instead, it states that auditors cannot form an audit opinion due to the absence or unavailability of sufficient appropriate audit evidence. With this opinion, auditors withdraw any responsibility that comes with auditing the financial statements.

Example

Given below is an example of the disclaimer of audit opinion for a client that auditors may provide.

Disclaimer of Opinion

We were engaged to audit the financial statements of Red Co., which comprise the statement of financial position as at December 31, 2021, and the statement of profit or loss and other comprehensive income, statement of changes in retained earnings and statement of cash flows for the year then ended, and notes to the financial statements, including a summary of significant accounting policies.

We do not express an opinion on the accompanying financial statements of Red Co. Because of the significance of the matter described in the Basis for Disclaimer of Opinion section of our report, we have not cannot obtain sufficient appropriate audit evidence to provide a basis for an audit opinion on these financial statements.

In the above example, the auditors state that they do not express an audit opinion on the subject matter. Therefore, it forms the disclaimer audit opinion. Auditors will provide their reasons for this opinion in the ‘Basis for Opinion’ paragraph.

Conclusion

Auditors reach a conclusion regarding an audit engagement and provide it in the form of an audit opinion. With the disclaimer audit opinion, auditors do not provide an audit opinion. Instead, they express that they were unable to obtain sufficient appropriate audit evidence. However, its impact must be pervasive, or else it would fall under a qualified audit opinion.

Further questions

What's your question? Ask it in the discussion forum

Have an answer to the questions below? Post it here or in the forum

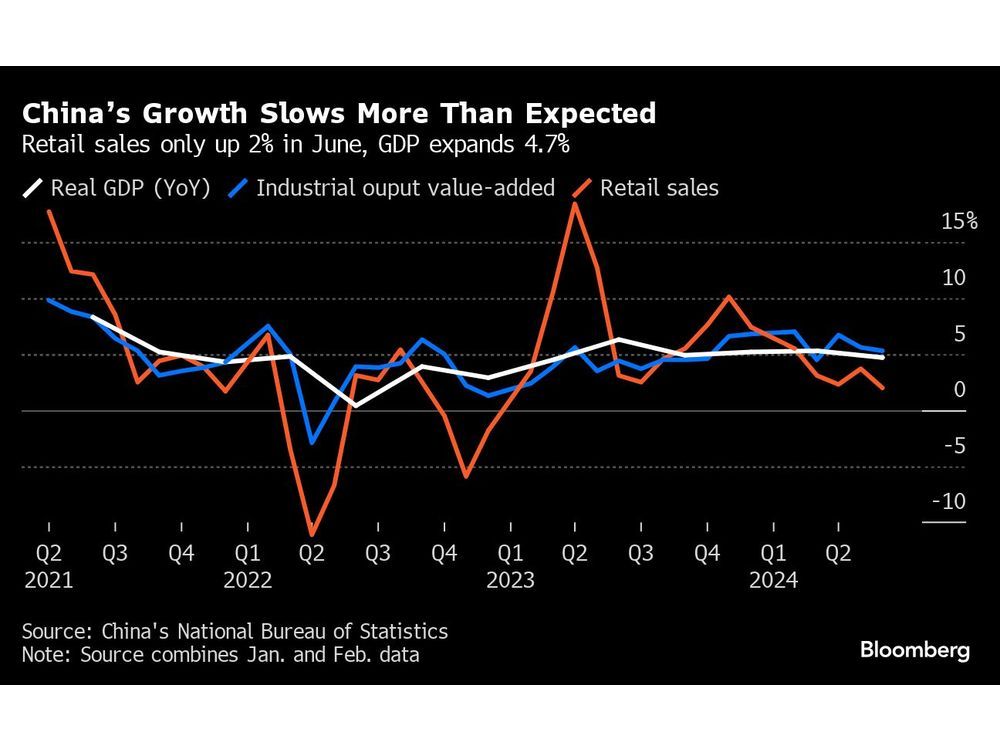

The runway toward a Federal Reserve interest-rate cut will come more into focus in the coming week amid fresh signs inflation is abating and economic activity is simmering down.

NEW YORK, July 20, 2024 (GLOBE NEWSWIRE) — Cell BioEngines, Inc., a New York, USA-based company researching stem cells in order to develop new cell therapies unlocked $1.75 million additional funds from SOSV and the Partnership Fund through the new therapeutics seed track, available for…

U.S. health officials advise people who are pregnant, elderly or have compromised immune systems to avoid eating sliced deli meat unless it's recooked at home to be steaming hot.

"By restricting the executive branch’s ability to craft and enforce regulations, the Supreme Court has opened the door to the Balkanization of the US economy."