Follow us on LinkedIn

Modern Portfolio Theory (MPT) is a theory developed by Harry Markowitz in 1952, which later earned him a Nobel Prize in Economics. The theory states that investors can create an ideal portfolio of investments that can provide them with maximum returns while also taking an optimal amount of risk. The theory helps risk-averse investors select a portfolio of investments while keeping their risks at an optimal level based on a given level of market risk.

While investors usually use the theory to increase or maximize their returns, it can also help them create a portfolio that minimizes their risks for a given level of expected return. Minimizing risks, however, may not result in the maximum amount of returns for investors. The main idea of the theory is diversification of portfolios, which in turn, results in decreased risks.

In a previous post, we provided a concrete example of MPT. In this post, we are going to discuss Modern Portfolio Theory in more detail.

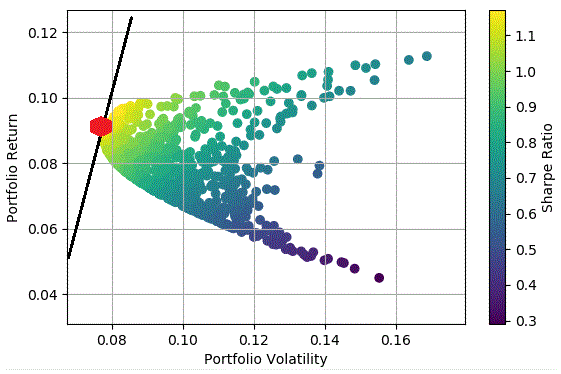

What is an efficient frontier?

The Modern Portfolio Theory introduces the concept of an efficient frontier, also known as a portfolio frontier. An efficient frontier represents a set of portfolios that maximize the expected returns for each level of risk or standard deviation. According to the theory, for every level of return that investors expect, there is an investment that can offer them the lowest standard deviation. Similarly, for every level of risk, there is a portfolio that gives the highest return.

By plotting together both combinations, investors can obtain a resulting line, known as the efficient frontier. The resulting line is in the shape of a curve. Portfolios in the upper part of the curve represent an efficient portfolio as it represents the maximum return for a given level of risk. Based on the expected level of risk, the position of the portfolio on the graph will change.

Advantages of Modern Portfolio Theory

There are certain advantages of the Modern Portfolio Theory. First of all, MPT helps investors evaluate and manage the risks and returns associated with their investments. Through this, investors can maximize their return based on the level of risk they are willing to take. Similarly, the theory promotes the idea of portfolio diversification, which can help investors reduce the chances of failure. When one investment fails, the others will likely perform better.

Disadvantages of Modern Portfolio Theory

The Modern Portfolio Theory also has some disadvantages. First of all, the theory requires investors to use historical information about companies or their investments. This historical information can not represent the current or future prospects of the company. Furthermore, the theory also makes several assumptions that lead to inaccurate results.

Assumptions of Modern Portfolio Theory

There are several assumptions that the theory makes. The most important assumption among them is the existence of a perfect or efficient market. These include further assumptions such as access to similar information to all market participants, no transaction costs, homogeneous products, no discrimination, etc. Perfect markets don’t exist, i.e. they are theoretical markets.

While these assumptions form the foundation of the theory, they can also prove to be misleading for investors. It is one of the reasons why experts around the world challenge or criticize MPT.

Conclusion

Modern Portfolio Theory (MPT) states that investors can construct an ideal portfolio of maximum returns for themselves at a given level of risk. The theory can also help investors in minimizing their risks. MPT supports the idea of portfolio diversification, and it can help investors with risk management. However, in practice, investors should pay attention to the underlying assumptions of the theory and its limitations.

Further questions

What's your question? Ask it in the discussion forum

Have an answer to the questions below? Post it here or in the forum

Citigroup on Friday posted second-quarter results that topped expectations for profit and revenue on a rebound in Wall Street activity.

JPMorgan Chase on Friday posted second-quarter profit and revenue that topped analysts' expectations as investment banking fees surged 52% from a year earlier.

NEW YORK — Announcement of Mesabi Trust Distribution The Trustees of Mesabi Trust (NYSE:MSB) declared a distribution of thirty cents ($0.30) per Unit of Beneficial Interest payable on August 20, 2024 to Mesabi Trust Unitholders of record at the close of business on July 30,…