Follow us on LinkedIn

What is a convertible bond?

A convertible bond (or preferred share) is a hybrid security, part debt and part equity. Its valuation is derived from both the level of interest rates and the price of the underlying equity. Several convertible bond pricing approaches are available to value these complex hybrid securities such as Binomial Tree, Partial Differential Equation and Monte Carlo simulation. One of the earliest approaches was the Binomial Tree model originally developed by Goldman Sachs [1,2] and this model allows for an efficient implementation with high accuracy. The Binomial Tree model is flexible enough to support the implementation of bespoke exotic features such as redemption and conversion by the issuer, lockout periods, conversion and retraction by the share owner etc.

In this post, we will summarize the key steps in valuing a convertible bond using the Binomial Tree approach. Detailed description of the method and examples are provided in References [1,2]. We also provide sample programs in Excel and Python for pricing a convertible bond. Download the excel workbook by following this link. Python program can be downloaded here.

Generally, the value of a convertible bond with embedded features depends on:

- The underlying common stock price

- Volatility of the common stock

- Dividend yield on the common stock

- The risk free interest rate

- The credit worthiness of the preferred share issuer

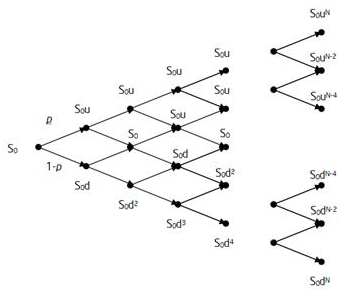

Convertible bond pricing using a binomial tree

Within the binomial tree framework, the common stock price at each node is described as

where S0 is the stock price at the valuation date; u and d are the up and down jump magnitudes. The superscript j refers to the time step and i to the jump. The up and down moves are calculated as

and

where  is the stock volatility, and

is the stock volatility, and  is the time step.

is the time step.

The risk neutral probability of the up move, u, is

and the probability the down move is 1-p

After building a binomial tree for the common stock price, the convertible bond price is then determined by starting at the end of the stock price tree where the payoff is known with certainty and going backward until the time zero (valuation date). At each node, Pj,i the value of the convertible is

where m denotes the conversion ratio.

If the bond is callable, the payoff at each node is

The payoff of a putable bond is

Here C and P are the call and put values respectively; r denotes the risk-free rate.

The above equations are the key algorithms in the binomial tree approach. However, there are several considerations that should be addressed due to the complexities of the derivative features

- Credit spreads (credit risk) of the issuers which usually are not constant.

- Interest rates can be stochastic.

- Discount rate ri,j depends on the conversion probability at each node. This is due to the fact that when the common share price is well below the strike, the preferred share behaves like a corporate bond and hence we need to discount with a risky curve. If the share is well above the strike then the preferred behaves like a common stock and the riskless curve need to be used.

- The notice period: the issuer tends to call the bond if the stock price is far enough above the conversion price such that a move below it is unlikely during the notice period. For most accurate results, the valuation would require a call adjustment factor. This factor is empirical and its value could be determined by calibration to stock historical data.

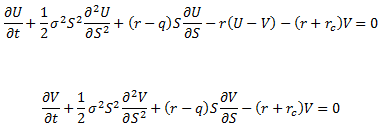

Convertible bond pricing using Partial Differential Equation (PDE) approach

An alternative way of pricing a convertible bond is to use the PDE method developed by K. Tsiveriotis and C. Fernandes [3]. In this method, we have to solve a system of coupled equations,

where U denotes the convertible bond’s price,

V is the value of the cash-only part,

S is the stock price,

r is the risk-free interest rate,

q denotes the dividend yield,

rc is the credit spread.

The above 2 equations can be solved simultaneously by using the Finite Difference Method in which the partial derivatives are approximated by finite differences.

Convertible bond pricing when there is a contingent convertible feature

A contingent convertible bond is defined with two elements: the trigger and the conversion rate. While the trigger is the pre-specified event causing the conversion process, the conversion rate is the actual rate at which debt is swapped for equity. The trigger, which can be bank specific, systemic, or dual, has to be defined in a way ensuring automatic and inviolable conversion. A possibility of a dynamic sequence exists—conversion occurs at different pre-specified thresholds of the trigger event. Since the trigger can be subject to accounting or market manipulation, a commonly used measure has been the market’s measure of bank’s solvency. The design of the trigger and the conversion rate are critical in the instrument’s effectiveness. Read more

From a quantitative point of view, modeling such a contingent conversion feature is far from trivial. Usually, the 20/30 contingent conversion can be modeled somewhat explicitly on the PDE lattice by introducing an extra state variable which tracks whether the condition was satisfied in the previous monitoring quarter. The soft call feature is often more material as it is in the interest of the issuer to call the bond as soon as the value equals the call price (plus accrued interest).

Readers who would like to learn more about the mathematical aspects of pricing a contingent convertible bond can start with the following articles:

Valuing convertible bonds with 20-of-30 soft call provision

Convertible bond pricing example

The binomial convertible bond pricing approach presented in the previous section can be implemented in scripting languages such as VBA or Matlab. Here we present a simple example of pricing a convertible bond in Excel. We are going to value a hypothetical convertible bond. The specifics of the hypothetical convertible bond are as follows

| INPUTS | |

| Stock price | 100 |

| Volatility | 0.25 |

| Risk Free Rate | 0.02 |

| Risky Rate (risk free+credit spread) | 0.08 |

| Coupon | 0.06 |

| Maturity (in years) | 5 |

| Conversion ratio | 10 |

Using the formula provided in the previous section, we calculated the up and down moves and the probability of the up move. The results are

| MODEL PARAMETERS | |

| dt | 1.00 |

| u | 1.28 |

| d | 0.78 |

| Probability Up | 0.48 |

Once the tree parameters are calculated, we next build the tree and then work backward from the end nodes in order to obtain the convertible bond’s price at time zero. As the final result, the bond price is $1319 (per $1000 notional)

Note that this is a simplified example. In real life, convertible bonds are usually more complex. They often include features such as call, put, contingency conversion options. The call and put options can be implemented using the formula given in the previous section.

A sample Excel workbook for pricing a convertible bond can be downloaded by following the instruction below. Also check out a follow-up post on convertible bond pricing in Python.

How to account for convertible bonds

A convertible bond is a type of bond that accompanies a right or obligation to receive a company’s stocks in the future. As the name suggests, a convertible bond allows investors to convert their bonds into ordinary shares. The issuer includes a condition with the convertible bond that specifies the number of shares that investors will receive for each bond.

Convertible bonds include all the characteristics of traditional bonds, such as maturity date and interest payments. As with other bonds, the issuer dictates the terms that investors will receive on their bonds. At maturity, the investor receives the bond’s face value. Unlike other bonds, however, they can also exercise their rights to convert their bonds into shares. In essence, investors can convert their bond investments into stocks.

How does accounting for convertible bonds work?

There are three stages to convertible bond accounting that issuers must perform. Firstly, the issuer must record the issue of bonds to investors. Once they do so, they must account for the coupon payments made to investors at predetermined times. Lastly, they must treat the settlement of the bond. The accounting for convertible bonds for each of these steps differ.

Issuance of convertible bonds

Convertible bonds include two portions. Firstly, it consists of an equity portion comprising the shares that investors will receive if they exercise their right to the shares. On the other hand, it also includes a liability component, like traditional bonds. Issuers must separate these components and record them separately.

Investors can calculate the liability portion by discounting the future cash flows from bonds. For that, they must use the rate of a similar debt instrument. This portion will comprise the liability component of the bond. The equity component will be the difference between the liability component’s value and the bond issuance proceeds. Once they do so, they can use the following accounting treatment to record the transaction.

| Dr | Cash/Bank |

| Cr | Liability portion of the convertible bond |

| Cr | Equity portion of the convertible bond |

Interest payments

Once an issuer issues the bonds to investors, they must make regular interest payments. The accounting treatment for interest payment transactions is similar to traditional bonds. Issuers must record the interest as an expense and any payments as a reduction in assets. The accounting treatment will be as follows.

| Dr | Interest expense |

| Cr | Cash/Bank |

Maturity of convertible bonds

Bond issuers also have to account for the bond at maturity. For traditional bonds, the accounting treatment is straightforward. For convertible bonds, however, the treatment will differ. It is because, at maturity, convertible bonds may get converted into stocks. Under each circumstance, the treatment will vary.

If investors do no exercise their option to convert, the issuer must decrease the associated liability with the convertible bond. In that case, the accounting treatment will be similar to other bonds, which is as below.

| Dr | Convertible bond (Liability) |

| Cr | Cash/Bank |

On the other hand, if investors choose to exercise their option to convert, the issuer must account for it differently. In that case, they must replace both the equity and liability portion of the bond with the issued shares. They can do so by using the following treatment.

| Dr | Convertible bond (Equity) |

| Dr | Convertible bond (Liability) |

| Cr | Share Capital/Premium |

In summary, convertible bonds differ from traditional bonds because they allow investors to convert their shares into stocks. The accounting for convertible bonds differs from other bonds. Like traditional bonds, issuers must account for convertible bonds at three stages. These include the issuance stage, interest payments, and maturity stage.

A SAMPLE EXCEL WORKBOOK FOR PRICING A CONVERTIBLE BOND CAN BE DOWNLOADED BY FOLLOWING THIS LINK.

References

[1] Valuing Convertible Bonds as Derivatives, Quantitative Strategies Research Notes, Goldman Sachs, November 1994.

[2] Pricing Convertible Bonds, Kevin B. Connolly, Wiley, 1998.

[3] Tsiveriotis, K. and Fernandes, C. (1998), Valuing Convertible Bonds with Credit Risk, Journal of Fixed Income, 8(2): pp. 95–102.

Further questions

What's your question? Ask it in the discussion forum

Have an answer to the questions below? Post it here or in the forum

The Princess of Wales will present the trophy to either last year's winner, Carlos Alcaraz, or seven-time Wimbledon champion, Novak Djokovic.

GOODS

Thanks

Great model.

Great. Neil