Follow us on LinkedIn

In the previous post, we introduced the Parkinson volatility estimator that takes into account the high and low prices of a stock. In this follow-up post, we present the Garman-Klass volatility estimator that uses not only the high and low but also the opening and closing prices.

Garman-Klass (GK) volatility estimator consists of using the returns of the open, high, low, and closing prices in its calculation. It is calculated as follow,

where hi denotes the daily high price, li is the daily low price, ci is the daily closing price and oi is the daily opening price.

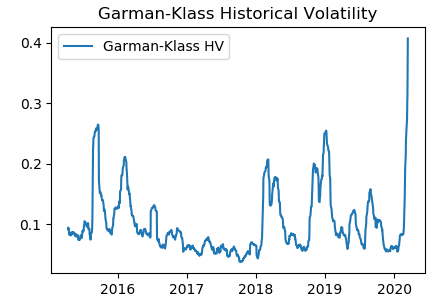

We implemented the above equation in Python. We downloaded SPY data from Yahoo finance and calculated GK historical volatility using the Python program. The picture below shows the GK historical volatility of SPY from March 2015 to March 2020.

The GK volatility estimator has the following characteristics [1]

Advantages

- It is up to eight times more efficient than the close-to-close estimator

- It makes the best use of the commonly available price information

Disadvantages

- It is even more biased than the Parkinson estimator

Also check out Historical Volatility Online Calculator.

References

[1] E. Sinclair, Volatility Trading, John Wiley & Sons, 2008

Further questions

What's your question? Ask it in the discussion forum

Have an answer to the questions below? Post it here or in the forum

Prime Minister Keir Starmer’s promise to “get Britain building again” will quickly face a shortage of skilled workers in the very industries he’s hoping will power the turnaround.